Why You Will Never Understand Blockchains

Spend any time researching blockchains, and you’ll be inundated with a host of benefits with the potential to impact nearly every aspect of our lives. Numerous articles highlight the technology’s ability to replace existing financial systems, revolutionize the delivery of content, tokenize physical assets, establish the provenance of digital assets, etc… All told, you’d think that this phenomenon has the potential to create billions (if not trillions) of economic value.

That’s where you’d be wrong.

While the applications being discussed today are compelling, I’d argue that they’ll amount to little more than a rounding error by the end of the century. Factoring in recent and projected advances in AI, IoT and Big Data, the potential impact of blockchains won’t be measured in billions or trillions, but in the QUADRILLIONS.

Skeptical that this nascent technology could generate that much value? You should be. Because blockchains weren’t designed for your tiny human brain — they were designed for the machines…

The Dawn of the “Intelligent Machine” Economy

In his book The Third Wave: An Entrepreneur’s Vision of the Future, former AOL chief Steve Case argues that the impact of digital technology on our economy has been relatively mild to date. While the internet has revolutionized how we shop, communicate and consume media, it’s not even close to reaching its full potential.

Over the next 10 to 20 years, we will likely see advances in IoT, AI and Big Data drive a new industrial revolution that permeates all sectors of our economy (and society). Some potential examples include:

- Agriculture: “Smart farms” will use remote sensors to monitor microclimates and detect irregular conditions, automated systems will synchronize water and fertilizer usage and robots will plant, nurture and harvest crops

- Logistics and Transportation: Fleets of autonomous vehicles will integrate with “smart” warehouses, track inventory with remote sensors and employ telematics to optimize routes and coordinate delivery times

- Healthcare: AI doctors will become commonplace, remotely monitoring a 24/7 stream of patient data gathered from wearables, instantly referencing this against a global reserve of medical knowledge and providing early warnings and highly-accurate diagnoses

- Energy: Utilities will relinquish control of the grid, using a combination of remote sensors and machine learning to automate their generation portfolios, coordinate distribution and remotely monitor and control energy consumption over a network of “smart homes” and buildings

Unlike previous industrial revolutions, the “Intelligent Machine Economy” will largely be self-governing, consisting of hundreds of billions of connected devices (e.g. “machines”) using artificial intelligence to automate nearly every aspect of our lives.

Running low on beer? No problem, your smart refrigerator will sense that and send a drone to pick up a six pack.

Infinite Complexity

While this is a promising vision, it’s also somewhat concerning.

Simple logic tells us that the more actors we have in an economic system, the more complex that system becomes. But many forget that this complexity grows at an exponential rate.

Robert Metcalfe illustrated this brilliantly with his eponymous law, which states that the number of potential relationships in a system is proportional to the square of the number of users of that system.

To put it in simpler terms — two telephones can make 1 connection, five can make 10 connections and twelve can make 66 connections.

Our world right now consists of 7 billion people — that’s 25 quintillion possible economic relationships with each connection representing the potential for multiple transactions.

That’s a big number, to be sure, but what happens if we imagine a world where hundreds of billions of additional economic actors are instantly added to the mix? Machines that can use some form of artificial intelligence to fashion their own relationships and conduct autonomous transactions…

As you might have guessed, things get complicated very fast. If research predicting over 100 billion connected devices using some form of machine learning by 2030 is correct, then we’re going to live in a world with 5 sextillion connections. If you believe Softbank’s estimate of 1 trillion connected devices, that number approaches a septillion.

While these numbers are hard to grasp because of their sheer size, the key takeaway here is that the impending increase in the number of commercial actors has the potential to make the global economic system up to 2,000,000% more complex than what we experience today.

So by 2030, we have the potential live in a world of nearly infinite complexity — billions to trillions of connected devices, consisting of sextillions to septillions of connections executing an untold number of transactions, all without potential human oversight.

Scary? It should be. It’s a concerning scenario that raises many questions including:

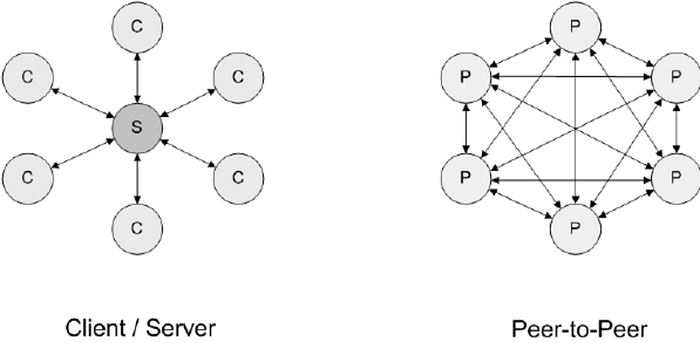

1. Can the existing client-server or cloud architectures handle that increase in volume?

2. Will centralized ecosystems, like the ones we have today, be able to maintain security? Or will the single point of failure serve as a giant “honeypot” for hackers?

3. Can we trust the autonomous actors in this economy? More importantly, can they trust each other?

4. Do we trust centralized entities (such as FAANGS) to administrate this system and prudently exercise what could become almost unlimited power?

I think that many would argue that the answer to one or all of these questions is a resounding “no”.

Fortunately, there’s an elegant solution to these problems, one that (perhaps unwittingly) comes from Satoshi.

Blockchains as the Neurons of the Global Brain

As a quick reminder, blockchains are so groundbreaking because they are the first technology to solve the Byzantine General’s Problem.

Prior to the creation of the genesis block, people had no way to organize large groups of strangers over vast distances without employing centralized authorities (e.g. governments, banks, churches) to establish trust and enforce rules.

The release of Bitcoin in 2009 created a new paradigm, eliminating the need for middlemen and creating the opportunity — for the first time in human history — to organize in a decentralized manner.

The importance of decentralized networks can’t be overstated, as they will serve as the foundation that creates scalability, security and trust in the Intelligent Machine economy.

Advantage #1: Scalability

As mentioned previously, the emergence of IoT could increase the complexity of our economy by several orders of magnitude, creating a situation where an incomprehensible volume of transactions need to be orchestrated, monitored and managed.

The systems we use today may find it difficult to handle this unprecedented increase in traffic as centralization itself creates a “bottleneck” in the network. Because client-server architectures tend to scale linearly — in other words, a given increase in traffic requires a similar increase in capacity on the server side — it is unlikely that they will be able to keep pace with the expected increase in demand without requiring massive investments in infrastructure (e.g. a LOT of new server farms in the desert).

Decentralized, peer-to-peer networks, on the other hand, can scale exponentially because each device can act as both a client and as a server and simultaneously initiate and fulfill requests from the other devices. This allows them to handle substantial amounts of traffic without sacrificing efficiency or requiring large investments of capital.

While it may seem ironic to list “scalability” as a benefit of blockchains given the current struggles today, the fact that they enable the creation of true peer-to-peer networks — solving the issues of trust, security and misaligned incentives that have plagued such systems in the past — is a critical feature and one that will likely help create a robust framework for scaling the highly complex ecosystems of tomorrow’s economy.

Advantage #2: Security

The centralized architecture that causes the scalability issues listed above also creates massive security risks by being reliant on a central point of failure — serving as a “honeypot” where nefarious actors (human or machine) can disable the whole network with a coordinated attack on one target.

Decentralized networks, on the other hand, are not reliant on a single central server to handle all processes. They mitigate this risk by employing millions of individual nodes. While a malicious actor can attack one, dozens or even hundreds of nodes, it’s unlikely that they will be able to shut down the majority of them.

Perhaps more importantly, a decentralized economy can serve as a hedge against something much scarier than hackers or malicious AI — control of the “global brain” by a cabal of global elites.

Because legacy systems require centralized authorities for trust, increases in usage tend to create “winner-take-all” markets that breed monopolies. Indeed, over the past decade we have seen the rise of FAANGS, a cabal that currently dominates over 70% of internet traffic, is expected to control 90% of the cloud and effectively has the power to control prices, censor content and shape culture.

Under the current paradigm, exponential increases in traffic would only serve to deepen this moat, creating the potential for an Orwellian future threatening our economic, political and cultural freedoms.

But once again, the proper use of blockchain technology eliminates the need for these gatekeepers, “defangs” FAANGS (or whatever succeeds them), democratizes the ecosystem and ultimately ensures security in an autonomous marketplace.

Advantage #3: Trust

Finally, trust will be paramount in the creation of the Intelligent Machine economy. A fully-automated ecosystem that exists with limited human oversight is a scary proposition that breeds a host of questions, including:

- How do we validate that the nodes and IoT devices are real?

- Will devices at the “edge” be more vulnerable to hacking?

- Can we verify that the data hasn’t been manipulated?

- How do we protect against malicious AI?

- Do we trust machine intelligence to behave to the best interest of society?

- How can we ensure that centralized entities don’t co-opt AI for their own purposes?

Again, two inherent properties of blockchains — trust through consensus and immutability — can ensure data integrity, audit the system’s thinking processes, help the nodes validate each other and facilitate machine-to-machine interaction, allowing autonomous participants to share information and synchronize decisions.

The $1,000,000,000,000,000,000,000,000 Machine

So what’s the takeaway here? How big can a blockchain-driven economy get?

Unfortunately, I don’t think I can answer that any more than a caveman could’ve predicted the effects of the industrial revolution.

But here are a few things to consider:

1/ Technological advancements throughout history have ignited exponential periods of global GDP growth, each seemingly larger than the last. Notable examples are:

- The development of machine tooling and steam power in the 18th and 19th centuries (~300% growth)

- The inventions of the telephone, light bulb, phonograph and the internal combustion engine around the turn of the 20th century (~800% growth)

- The introduction of the personal computer, internet and information technology at the latter half of the 20th century (~1,400% growth)

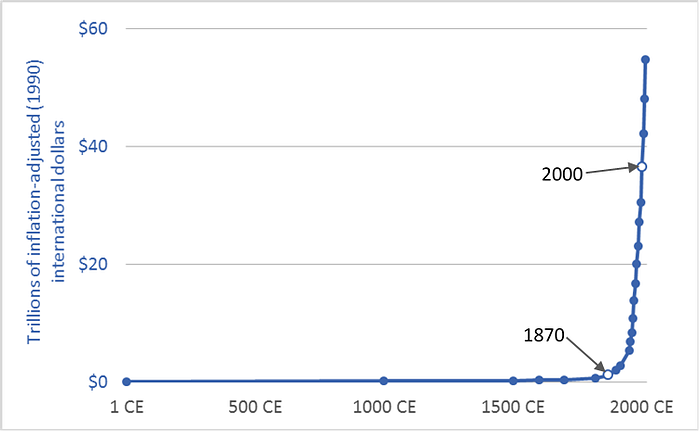

2/ Starting from Year 0, it took roughly 1,500 years for World GDP to double. Now it doubles every twenty years.

3/ Applying Metcalfe’s law, although perhaps crude and inaccurate, to 100 billion new economic actors yields a global GDP of almost 18 quadrillion, (a 20,000% increase over today)

So is it ridiculous to assume that the refinement of artificial intelligence, the internet of things and blockchains could result in an expansion that transcends anything we’ve previously seen?

Perhaps, but I would’ve also probably been laughed at for showing this chart in the late 1800s:

While I’m not smart enough to even begin to warrant a guess on the exact value of a tokenized economy, I am humble enough to acknowledge that it may be much, much, much bigger than we can imagine.

After all, an “Intelligent Machine” economy has the potential to upend thousands of years of human history and drive value in ways we can’t even imagine.

And blockchains will be the “glue” that holds that economy together.